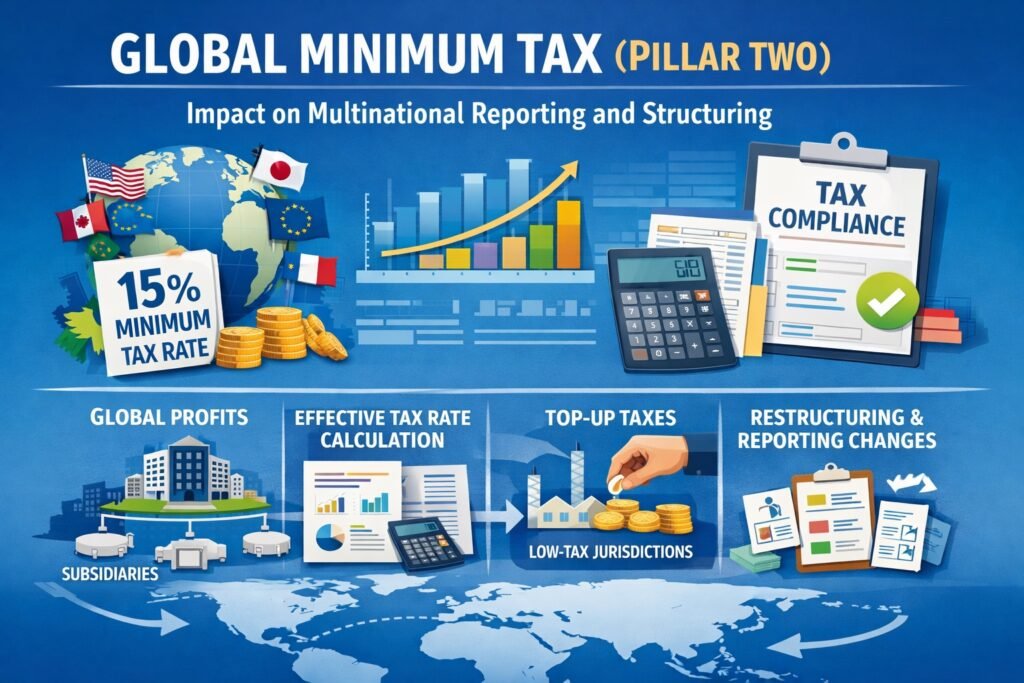

The Global Minimum Tax, often called Pillar Two, is a set of international tax rules designed to make sure large multinational companies pay at least a minimum level of tax, usually around 15%, in every country where they operate. Governments introduced it to reduce profit shifting, where companies move income to low-tax countries to lower their overall tax bill. Under these rules, if a company’s income in one country is taxed below the minimum rate, another country — often where the parent company is located — can apply a “top-up” tax to reach the minimum level.

For multinational reporting, this means companies must now track their profits, taxes paid, and financial data country by country with much greater detail. Existing financial statements alone are not enough; firms need new calculations based on adjusted accounting income and special tax rules. This increases compliance work, requires changes to reporting systems, and often forces closer coordination between tax, finance, and legal teams.

For corporate structuring, Pillar Two reduces the benefit of routing profits through low-tax jurisdictions. Many tax planning strategies that relied on tax havens are now less effective because the minimum tax removes the advantage. As a result, multinationals are reviewing where they hold intellectual property, financing hubs, and regional headquarters, focusing more on business reasons such as operations, talent, and regulation rather than purely tax savings.